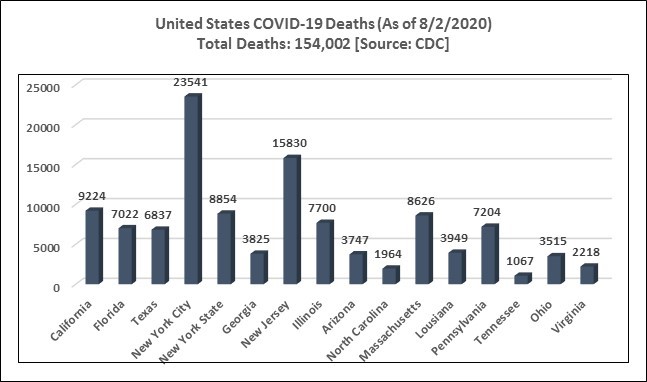

Recap: Financial markets were in a tug of war during July as investors weighed encouraging vaccine news and hoping for new economic stimulus against indications that the recovery might be stalling. The pandemic has marked another gloomy milestone in the U.S. as confirmed coronavirus cases approached the five million mark. With cases continuing to soar in several states, reopening plans have been increasingly rolled back and restrictive measures reintroduced to help curb the spread.

The surge in infections is weighing on economic activity. Real GDP has contracted a record-breaking 32.9% annualized in the second quarter, or a 9.5% drop compared with the same quarter a year ago. The level of GDP is now 10.8% below its 2019 Q4 level.

The rollback has also started to come through in high-frequency indicators. Initial jobless claims, which had declined for fifteen straight weeks, rose for the second week ending on July 25, and the number of people receiving unemployment benefits has increased to 17 million, signs that jobs recovery is losing momentum.

On a more positive note, the U.S. housing market has showcased a recovery that appears to be stronger than other areas of the economy. With risks increasingly tilted to the downside, policymakers have been working on the next set of measures to help support the economy.

The U.S. economy faces a long road to recovery that will require greater public vigilance to prevent the spread of the coronavirus pandemic and more spending from Congress.

GDP: The U.S. economy registered its worst decline in the second quarter. If not for the stimulus the government provided in response to the Covid-19 crisis, it would have been worse. Parsing through the national accounts data has revealed a broad-based weakness in most of the spending components of GDP in the second quarter, which comes as little surprise given that the economy was more or less shut down from mid-March through mid-May. The fall in activity was led by a 35% (annualized) decline in real personal consumption expenditures. Non-residential fixed investment fell 27%. International trade similarly fell off a cliff, with exports down 64% and imports down 53%. The only major component of GDP to grow in the second quarter was government spending.

Growth is expected in real GDP in Q4 and 2021 but that will depend on the course of the spread of the virus. Until a vaccine has been found and distributed, certain economic activity will remain restricted. Maintaining the financial health of businesses and households through this period will require ongoing monetary and fiscal policy supports. A pullback of these supports has remained a considerable downside risk to the recovery.

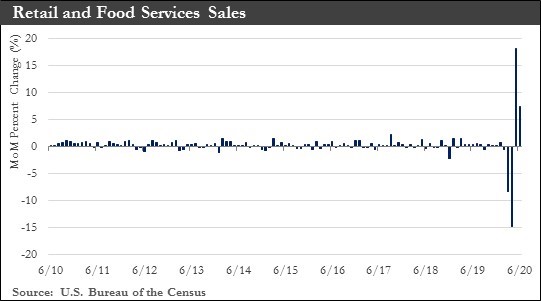

Retail Sales: Following a surge in May, retail sales continued to rise in June, posting a 7.5% month-on-month gain. Retail sales have now recovered almost all the lost ground since the closures of non-essential businesses in March and April.

The strength in retail spending, despite a double-digit unemployment rate, has been thanks to income support established in the CARES Act. These measures have more than offset the loss of employment income for most households. Congress will need to work on a new deal to provide additional support to households. Without it, consumers will likely tighten purse strings and retail sales could again see declines in the months ahead.

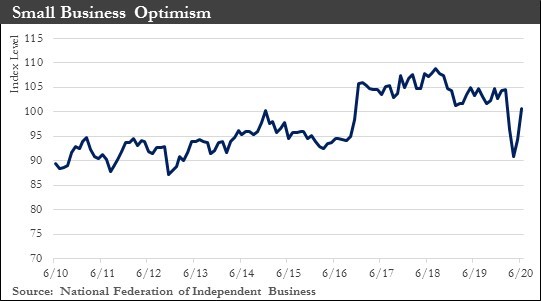

Small Business: The NFIB's small business optimism index increased by 6.2 points to 100.6 in June. The improvement was broad-based with eight of the ten subcomponents advancing in the month. The increases were led by real sales expectations after three consecutive months in negative territory.

Small business confidence has now improved for two straight months, reflecting the rebound in economic activity that ensued as states eased restrictions and stay-at-home orders were lifted across the country. Programs such as the Paycheck Protection Program (PPP) played a key role in helping small businesses stay afloat during these trying times. More support will likely be needed to sustain the recovery.

Inflation: Consumer prices rose 0.6% month-over-month in June, the first increase since COVID-19 hit. Total CPI was up 0.6% year-on-year and energy prices increased for the first time in six months. After three consecutive months of declines, core prices rose 0.2% m/m in June. As a result, core inflation was 1.2% on a year/year basis.Reduced demand has dramatically lowered inflation pressures. Therefore, the Federal Reserve acted decisively early in the crisis to stave off the risk of a deflationary trap. June's data has provided evidence that some of these deflationary forces have receded.

Accelerating COVID-19 cases, however, do present a serious downside risk. With shutdownsreturning across many parts of the country, prices may see renewed downward pressure. All told, inflation is expected to remain muted in the near future.

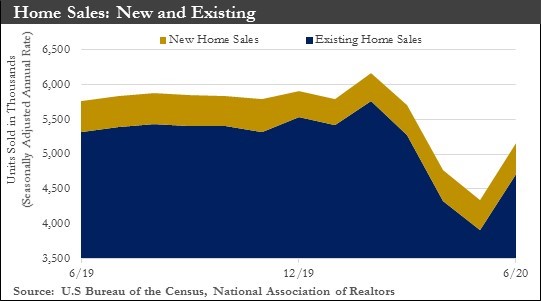

Housing: The housing sector has showcased a recovery that appears to be stronger than other areas of the economy. Housing starts increased by 17% month-over-month in June. By contrast, building permits rose by a much more modest 2%. Sales of new homes rose a sharp 14% in June, the second straight increase after two months. Sales of previously owned homes rose 21% in June over the prior month. Even with the jump in home sales, monthly activity has remained well below levels that were seen before the spring lockdowns. Many potential buyers have remained on the sidelines, concerned about job security or health risks related to visiting homes.

While improving economic conditions, solid demand and a low mortgage rate backdrop should support a continued recovery in the housing market, the road ahead is unlikely to be smooth. In the near-term, the strongest headwinds will come from the recent surge in infections, which has already prompted the reintroduction of restrictive measures in several states.

Labor Market: The U.S. labor-market recovery has lost momentum as a surge in coronavirus cases triggered heightened employer uncertainty and consumer caution. Filings for weekly unemployment benefits rose in the week ending July 25th as some states rolled back reopening because of the coronavirus pandemic, a sign the jobs recovery could be faltering. The elevated level of claims indicated many workers were being laid off, perhaps for a second time. Initial unemployment claims rose to 1.4 million for the week ending July 18th halting what had been a steady descent from the peak in late March, when the pandemic and business closures shut down parts of the U.S. economy.

The data has also shown that unemployment rolls have shrunk in recent weeks. Taken together, claims and benefits total suggested new layoffs are being offset by hiring and employers recalling workers, though at a slower pace than a few weeks ago.

Both job openings and postings in most industries in July have been down from June across the U.S. The labor-market slowdown has been widespread across industries and states, showing the economic turmoil is not limited to states in the South and West that are seeing the greatest increases in illness. It is still unclear how many of the job losses during the pandemic will become permanent.

Eurozone: In recent weeks, the prospects for the Eurozone have improved as COVID-19 case growth continued to stabilize and some economic indicators have been more encouraging, signaling that the worst may be over for the economy. Confidence surveys rebounded more than expected in June.

May retail sales jumped 18% month-over-month, the largest increase since the series began in 1999. Retail sales surged in almost all regions, but countries with milder lockdown procedures saw the largest gains. Given the large bounce back in May retail sales, the Q2 decline in services output, and thus GDP, could be milder than previously anticipated. Given a stronger starting point, a faster rebound in Q3 GDP is also possible.

Given these developments, there has been growing confidence in the Eurozone economy, under the assumption that the COVID-19 pandemic remains under control and data continue to improve. A smaller Q2 GDP fall and faster Q3 GDP rebound are expected. An 8% GDP decline for the full-year 2020 GDP remains a possibility.

Risks around this forecast are balanced as of now; however, progress could be made towards additional fiscal spending, which, if implemented, could support the Eurozone economy even further and help in the recovery.

China: China experienced a robust rebound in the second quarter, avoiding a recession and putting the economy back on a growth trajectory even as other countries struggled with the impact of the coronavirus pandemic. China’s economy grew by 3.2% in the second quarter compared to the same period a year earlier. The figure served as evidence that Beijing’s aggressive efforts to rein in the pandemic at home—though agonizing in the short term—has begun to restore longer-term business confidence. Industrial production and exports have been bright spots.

Despite the positive signals, there are plenty of causes for concern in the data. While factories are humming again and investment dollars are flowing into the economy, Chinese consumers—a far more important component of China’s economy than in previous downturns—have so far kept their wallets closed. Retail sales have fallen each month this year, a reflection of lingering concerns about public health and lost income during the worst of the lockdown between January and April.

The question now is whether China has seen the best of the recovery, as Beijing faces a daunting set of challenges through the end of the year: a coronavirus resurgence in the U.S. that could slow the global economy, increased tensions with Washington and widespread flooding and diminished buying power at home.

Outlook: The nascent U.S. recovery is already being threatened by a surge in new coronavirus cases. This has caused several states to either pause or roll back their reopening plans in recent weeks. There is little doubt that the economic outlook is largely going to depend on how successfully the pandemic is contained in the months ahead.

While May and June's economic figures benefitted from low-base effects as well as a gradual loosening of stay-at-home orders in many parts of the country, August and the following months will not have the same wind in their sails. The “easy gains” that were made possible from sharply curtailed spending have already been realized.

Real GDP will likely decline at a low rate in Q3-2020—roughly 3% at an annualized rate. Looking into 2021, the eventual development of an effective vaccine will allow economic life to gradually return to some semblance of “normal.” That said, it likely will take a few years before the economy bounces back to the level that prevailed before the pandemic struck. The level of GDP by Q4-2021 will likely still be roughly 3% below its Q4-2019 peak.

With the process of re-opening being delayed, employment growth likely will slow significantly in the coming months. The unemployment rate should fall to about 8-9% by the end of this year and to 6% or so by the end of 2021. This would imply that payrolls at the end of next year will still be more than seven million smaller than they were in February of 2020. An effective vaccine that is developed more quickly than anticipated, could lead to some faster job growth later this year and early next year.

With an elevated rate of unemployment and with inflation still benign—the rate of PCE inflation, the Fed’s preferred inflation measure, should remain well below the target of 2% throughout the end of next year.

The Fed is not expected to cut rates into negative territory. The FOMC is likely to keep its target range for the federal funds rate at 0.00% to 0.25% through at least the end of 2021. Consequently, long-term interest rates are likely to remain extraordinarily low.

Further financial assistance from Washington should be forthcoming to deal with state unemployment benefits, assistance for states and localities, and potentially an extension with further tweaks to the PPP program. Together these could help to cushion the now worsening blow to many areas of the economy that will continue until the pandemic is contained.

This Newsletter was produced for Middleburg Financial by Capital Market Consultants, Inc.

Sources: Federal Reserve of Chicago, Bloomberg, Department of Labor, Department of Commerce, Morningstar, National Federation of Independent Business, John Hopkins University, Eurostat

Disclosures:

Past performance quoted is past performance and is not a guarantee of future results. Portfolio diversification does not guarantee investment returns and does not eliminate the risk of loss. The opinions and estimates put forth constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Securities are not insured by FDIC or any other government agency, are not bank guaranteed, are not deposits or a condition to any banking service or activity, are subject to risk and may lose value, including the possible loss of principal.