Your Wealth

October 2020 Global Market & Economic Outlook

10.14.20

Recap: After a rollercoaster ride in the spring and summer, the U.S. economy appears to be entering a flatter stretch of renewal ahead of the pivotal 2020 presidential election. The thundering economic rebound following a historic recession in the wake of the coronavirus pandemic has shifted into a more lukewarm recovery. Consumer spending has slowed, business investment has softened, and the number of people going back to work has tapered off.

A slower recovery has been evident in the number of people applying for unemployment benefits. After falling through most of the summer, new state and federal jobless claims appeared stuck around 1.4 million or so a week. More big companies have announced layoffs and thousands of small businesses have closed permanently.

The spate of layoff announcements and persistently high unemployment seems to have dampened the optimism of consumers. With confidence shaken, so many people out of work, and the coronavirus still spreading, the U.S. cannot recover more rapidly. Many businesses have faced ongoing restrictions on occupancy while millions of Americans have continued to practice social distancing and shunned normally crowded places.

As gains in confidence have slowed, consumers have tightened their wallets, directly affecting consumer spending, in turn making it harder for businesses to justify adding to or even maintaining their current workforces.

The end of massive federal aid for the unemployed and small businesses also appears to have tapped the brakes on the speed of the recovery. The economy did not suffer as badly as many predicted when federal aid dried up, but incomes for millions of Americans were sharply reduced and some businesses were left high and dry.

The odds of additional government help before the November election seems unlikely. Democrats and Republicans have been sharply divided over how much to spend and have made no headway in negotiations since the last aid package expired in July.

So, what is going to get the economy moving faster or keep it growing?

A declining number of coronavirus cases has allowed states to ease restrictions and give businesses more leeway to operate. Schools, colleges, and other organizations, meanwhile, have tried to reopen and return to some semblance of normalcy.

The Federal Reserve, for its part, made it quite clear that it plans to keep U.S. interest rates at a record low for at least three more years — if not longer. And most importantly, people have gone back to work. Not as fast as they did earlier in the recovery, but the economy is still adding more jobs than it is losing.

If that is the case, the U.S. is unlikely to slip back into another economic malaise.

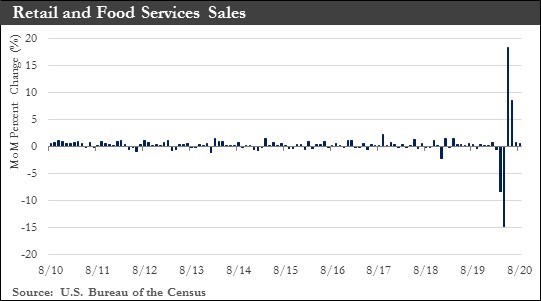

Retail Sales: Retail sales have continued to move up as consumers kept spending in August. Retail sales advanced 0.6% month-over-month in August, down from 0.9% in July. The monthly gain came as employers added jobs, the unemployment rate declined, and manufacturing output picked up. Consumers increased spending despite the expiration of some extra pandemic-related unemployment benefits, though future spending will be damped by benefit reductions.

However, the extraordinary gains in May and June have now given way to a much slower pace of spending. There have been two factors behind the flattening trend in retail sales growth.

First, a normalization of spending growth to historical trends as pent-up demand from the lockdowns has been satisfied. And second, incomes have declined for a significant share of the population as the $600/week payments provided by the CARES Act stopped in late July. This drop off in payments will surely stretch household finances.

Negotiations for a new stimulus bill have stalled in recent weeks. A lack of financial support could mean a decline in spending in the coming months. Aside from the pandemic, this has been the most significant near-term risk to the U.S. economic outlook.

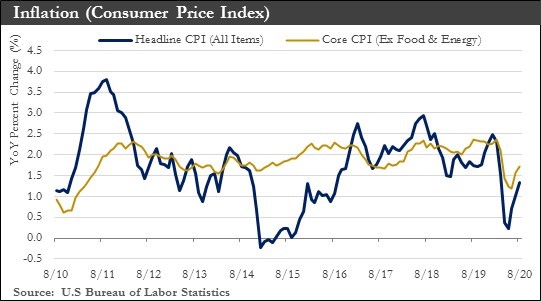

Inflation: U.S. consumer prices rose in August due to higher costs for a range of items, a sign of firmer inflation as demand for goods continues to rebound from a coronavirus pandemic-induced downturn earlier this year. The consumer-price index climbed a seasonally adjusted 0.4% in August. That marked the third straight month of gains for consumer prices, after sharp declines at the pandemic’s onset. Core prices increased by 0.4%.

The bounce back in consumer prices over the summer came as states reopened their economies and weathered a resurgence in coronavirus cases. Prices for certain goods have rebounded especially well, reflecting a shift in consumer habits and preferences amid the pandemic, as well as continued business disruptions and adaptations in many industries.

Longer-term trends have suggested inflationary pressures are muted, however. On a non-seasonally adjusted basis, the overall consumer-price index rose 1.3% in August from a year earlier and core prices increased 1.7% over the year. The Federal Reserve, acknowledging that inflation has mostly remained below its 2% target for several years, recently changed its policy framework to no longer pre-emptively lift interest rates to prevent higher inflation.

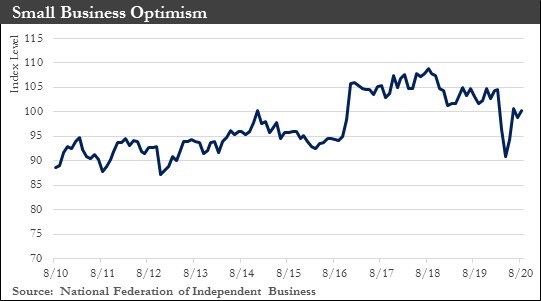

Small Business: The NFIB's small business optimism index increased by 1.4 points to 100.2 in August. Seven of the ten subcomponents improved in the month, two declined, and one remained unchanged.

Despite the improvement, the challenging economic conditions small businesses have operated under were front and center in the August report. With pandemic-related uncertainty elevated, expectations regarding future economic conditions kept deteriorating while real sales expectations continued to fall.

As more people return to work and in-person schooling resumes across the country, a resurgence in infections in the fall could further weigh on business investment and consumer spending. Also, stalled negotiations over the next installment of coronavirus relief measures in Washington tilt near-term risks to the downside. In that regard, the upcoming months will be key in shaping the path of a return to economic normalcy.

ISM Manufacturing: U.S. industrial production rose for the fourth consecutive month in August but at a much lower rate than earlier in the summer, a sign that the manufacturing recovery is slowing. It also highlights that overall demand remains weak and businesses are perhaps not fully convinced that the current recovery is sustainable.

In the near term, however, the manufacturing sector’s prospects continue to look good relative to many parts of the service sector, which has remained constrained by its reliance on in-person interaction. The ongoing need for social distance has shifted spending away from in-person services toward goods, as exhibited by recent movements in the new orders component of the ISM indices. But looking ahead, as the pandemic drags on, lingering softness in sales and an uncertain global outlook will weigh on capital spending, so manufacturers—even those tied most tightly to goods—are hardly in the clear.

Labor Market: The September employment report was encouraging, showing the U.S. labor market has continued to heal and remained firmly on a recovery path. That said, the pace of hiring has slowed and the trajectory of the recovery going forward will be heavily dependent on the coronavirus pandemic.

Remaining historically elevated, initial, and continuing jobless claims’ performance have also continued to signal ongoing strains in the labor market. There have been around 29-million workers receiving some form of jobless benefits. The increase in the number of job postings, a real-time measure of labor-market activity, has slowed dramatically since late July. The flattening trend in postings reflects a recent slowdown in demand for workers in some consumer-facing industries, such as foodservice and retail. The data has been consistent with other measures showing that while the labor market is still improving, the pace of gains appeared to be slowing. Moreover, the potential for new virus outbreaks this fall, and winter could be a downside risk to the labor market outlook.

Federal Reserve: In August, the Fed announced a new policy framework that abandoned the longtime strategy of pre-emptively lifting interest rates to head off higher inflation rates. It was an effort to fight the stubbornly low inflation that has persisted for the last decade. The Fed has tried to reset inflation expectations. For market participants, the key takeaway has been that the policy interest rate will remain lower for even longer relative to the Fed’s prior approach. Short term interest rates should be anchored near zero at least through 2023.

Eurozone: The COVID-19 outbreak and associated lockdown measures took a severe toll on the Eurozone economy in early 2020 as GDP slumped 15% in the first half of the year. However, since spring the outlook has become increasingly more hopeful given the actions of monetary and fiscal policymakers, and as activity data and confidence surveys have shown a relatively quick initial rebound from the deep downturn.

However, that more hopeful outlook has faced some questions in recent weeks. Retail sales unexpectedly declined in July, while the August services Purchasing Managers Index (PMI) dipped sharply to 50.5. Meanwhile, after the spread of COVID-19 slowed across the Eurozone during the summer months, the daily increase in new cases has jumped again as fall approaches and has been above the peak seen in March/April.

Against this backdrop, Eurozone September services PMI has shown further weakness, falling into contraction territory at 47.6. The Eurozone manufacturing PMI fared better, rising to 53.7.

European governments will be hesitant to re-impose the widespread, large-scale lockdown measures seen earlier this year. That said, less confident businesses and households, and the potential imposition of further partial restrictions could present downside risks to the outlook for the Eurozone. Specifically, the risks to the GDP growth outlook of 8% quarter-over-quarter for Q3-2020 and the longer-term forecast of a 5.0% increase for the calendar year 2021, are both tilted to the downside. There is also a risk that the euro appreciates even more gradually than currently expected over the medium-term.

Outlook: The U.S. economy continued its steady recovery from the sharp declines in the second quarter as demand and output strengthened. U.S. service-sector and manufacturing companies reported solid growth in September, a positive signal for overall economic growth in the third quarter.

The question now turns to whether the economy’s strong performance can be sustained into the fourth quarter. Coronavirus infection rates remain high in the U.S., and mounting uncertainty over the presidential election could further push down business optimism.

The path ahead continues to be highly uncertain. A full recovery is likely to come only when people are confident that it is safe to re-engage in a broad range of activities.

Based on recent data, after an initial plunge, households have been more than willing to increase spending on durable goods – suggesting little permanent damage to household confidence. Rather, what is holding back a broader recovery are the service-sector areas of the economy where the activity is directly impacted by the potential risk of infection. This offers a reason to expect a solid bounce back once these fears are allayed.

The case for a rapid return to the pre-pandemic economy has rested on businesses quickly hiring back workers laid off in the spring. And indeed, since April, the number of people on temporary layoff has plummeted by two-thirds, or about 12 million. But the longer the pandemic drags on, the more businesses in the most vulnerable sectors will close forever. Since February, more than two million people have permanently lost their jobs, and their numbers seem certain to grow.

With pandemic-related uncertainty remaining elevated, near-term risks to the economy still appear tilted to the downside. As such, continued government support will be essential in limiting financial stress to households and businesses and in determining the pace of the recovery.

Considering stalled negotiations around the next stimulus package in Washington, consumption growth is at risk of tapering off in the coming months. It is going to be a long and bumpy road back to economic normalcy.

Assuming no major second wave of the virus leads to another round of shutdowns, it is reasonable to expect the American economy to recover much of what was lost to the pandemic over the past year. While growth appears likely to slow after its initial burst on reopening, it should pick up again once a vaccine is available.

As a result, GDP is expected to regain its pre-recession level by the first quarter of 2022.

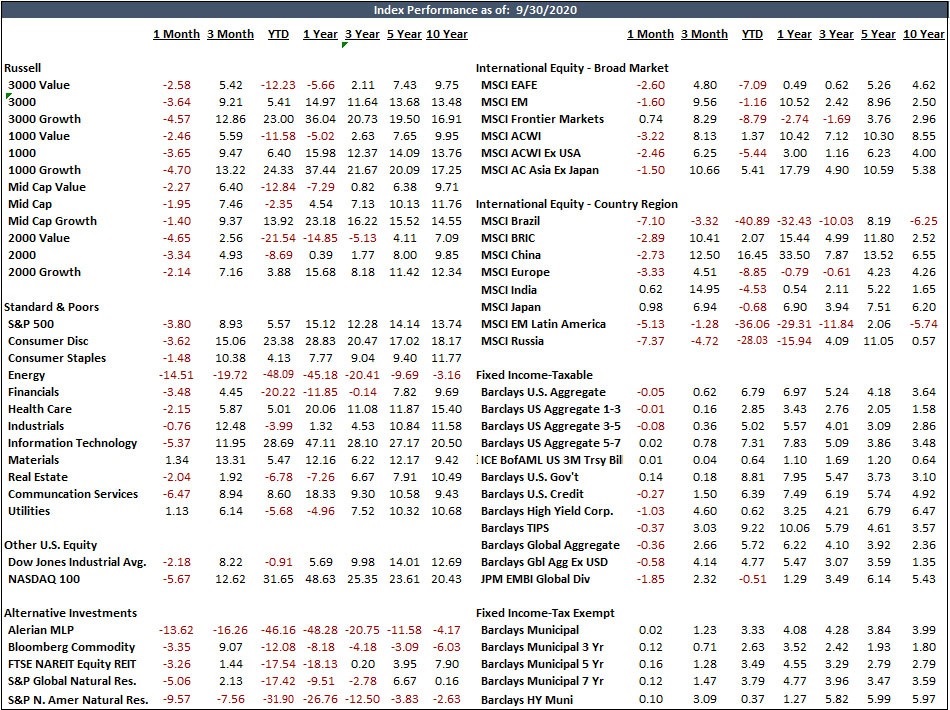

Recap: The economic recovery remained on track through the third quarter as macro data generally was positive and business and consumer confidence gained momentum. According to the third estimate of GDP released by the Bureau of Economic Analysis, U.S. economic activity experienced its largest contraction ever in the second quarter of 2020. When announced at the end of October, the third-quarter GDP is likely to reflect a sharp increase in the range of 20% to 30%. Despite this large and expected bounce, the economic recovery is likely to be more gradual, going forward. The shape of the recovery has been the subject of much debate. During the early days of the pandemic, there was hopeful talk about a “V” shaped recovery. More recently, economists have been suggesting a “K” shaped recovery is more realistic as it appears middle and upper-class workers have recovered quicker than individuals holding lower-paying jobs. The COVID-19 pandemic continued to dominate the news and strongly impact the path of recovery as well as market action during the third quarter. Until a vaccine is widely available, further disruptions and volatility are probable. Significant tailwinds in the third quarter were provided by the government’s ongoing and aggressive fiscal and monetary response to the COVID-19 pandemic. Given this environment, the S&P 500 rose 8.9% during the quarter. Overseas, the MSCI EAFE Index gained 4.8%, and the MSCI Emerging Markets Index increased by 9.6%. Fixed income markets produced positive returns. The Barclays U.S. Aggregate Bond Index gained 0.62% while the Barclays Global Aggregate ex USD Bond Index jumped 4.1%.

Domestic Equities: Despite the ongoing pandemic, U.S. equity markets continued to rebound during the first two months of the quarter. The tech-heavy Nasdaq Composite ran up nearly 20% through September 2nd to an all-time high before giving up a portion of these gains and ending the quarter with an 11% gain. Market volatility spiked in the final month of the quarter as investors focused on the reacceleration of positive COVID-19 tests along with indicators that a vaccine will likely not be available until the summer of 2021. Additionally, a vacancy in the Supreme Court ramped up the already contentious political climate and made a deal for additional fiscal stimulus less likely, or at least delayed. The possibility of a contested election is another source of uncertainty.

Throughout the quarter, the rising stock market has been at least partially driven by the federal government’s aggressive efforts to ensure that the capital markets remain liquid and investors stay confident. The Federal Reserve’s balance sheet now stands at more than $7 trillion, or about 80% higher than this time last year.

International Equities: Overseas, investor optimism rebounded with less vigor than in the U.S., especially in Europe where the economy contracted even more severely during the COVID-19 shutdowns. Additionally, a new spike in cases in Europe is fanning fears of a second wave of the pandemic. While it is probable that governments will be better prepared for a recurrence, the effects on consumer confidence and economic activity could be severe. As in the U.S., central bank accommodation and government stimulus have played an important role in stabilizing international economies. Corporate earnings growth was sharply negative during the quarter, but generally better than expected. The earnings outlook remains highly uncertain as company management teams are noncommittal in their guidance and, at best, are providing only short-term outlooks. Emerging market stocks registered a strong return in the third quarter, boosted by optimism toward progress on a COVID-19 vaccine and the ongoing economic recovery.

Fixed Income: The overall environment was largely "risk-on" during the quarter, although September was more muted amid rising COVID-19 infection rates and renewed lockdowns in some countries. Government bond yields were mixed, with the U.S. 10-year yield rising 3 bps, the UK 10-year yield increasing 6 bps, and the German 10-year yield falling 7 bps. Corporate bonds outperformed government issues with U.S. high yield issues gaining 4.6%. International bonds outpaced domestic issues as foreign currencies exhibited strength, relative to the U.S. dollar.

Outlook: In the U.S., supportive monetary and fiscal policies, the potential of a COVID-19 vaccine, and favorable fundamentals anchored by modest inflation are among factors supportive of domestic equities. The early recovery phase of the business cycle, typically characterized by low inflation and interest rates, usually favors equities over bonds. But after the dramatic rebound from the March 23rd lows, an equity market pullback would not be surprising. Volatility is expected to remain elevated into the new year for as long as the duration and impact of COVID-19 remain uncertain. Uncertainties surround the U.S. election, particularly as they may impact tax policy, government regulation, and the re-escalation of U.S.-China trade tensions. A victory by President Trump would likely benefit domestic equities as tax hikes would be averted while a Biden administration would probably benefit international stocks as trade policy may be less contentious. A contested election also has the potential to destabilize markets. In terms of cap and style, the markets may be poised for a rotation away from growth leadership toward more cyclical and value stocks given the potential for positive cyclical catalysts and extreme discounts in valuations. Shares of small-cap companies may also enjoy a strong recovery as the economy emerges from recession.

If the post-coronavirus economic recovery favors undervalued cyclical value stocks over expensive technology and growth stocks, developed international equities should perform well as major foreign stock indexes are overweight cyclical value stocks, relative to the U.S. In Europe, economic indicators have rebounded through the September quarter following the easing of lockdowns. COVID-19 infections have been rising, but hospitalization and death rates remain low. The prospect of nationwide shutdowns appears low. The MSCI EMU index, with its exposure to financials and cyclically sensitive sectors, has the potential to outperform when economic activity picks up and yield curves steepen. In Japan, the economy continues to lag the recovery of other major regions. Prime Minister Yoshihide Suga is expected to continue to the policies of his predecessor, Prime Minister Shinzo Abe, and has indicated he will provide further fiscal support before the year-end. Despite this support, the Japanese economy may remain a laggard in the recovery, due to constrained monetary policy and deflationary dynamics. In the UK, Brexit dominates the outlook, and the risk of a hard exit is high.

In emerging markets, uncertainties surrounding global trade policies will likely remain a headwind until investors get clarity about the state of trade negotiations after the U.S. election. COVID-19 is also a headwind as many emerging market economies are still battling to contain the virus outbreak and lack policy space to cushion the blow. Rhetoric has been escalating between the U.S. and China. Relative to the U.S., there is value in emerging market equities, and China’s early exit from lockdown measures as well as stimulus support should benefit the asset class. It is becoming clear that the lifting of lockdowns and government stimulus are the most important elements in determining how economies recover from the current health crisis. Unfortunately, the pandemic has caused almost all developing countries to experience a deterioration of budget balances and rising debt-to-GDP ratios. This weaker fiscal position makes emerging markets more vulnerable.

For fixed-income investors, the environment remains relatively challenging with yields on 10-year Treasuries ending the quarter around 0.68%. Given the Fed's commitment to a "lower for longer" rate policy, the yield on the 10-year Treasury is expected to remain below 1.0% for the foreseeable future. The fall election may prove to be a catalyst for rate moves, particularly if a Democratic sweep becomes reality. Markets would likely perceive this to be a risk-off event, driving yields lower. U.S. investment-grade credit issues have seen spreads narrow. Valuations in this asset class appear a bit rich. Investment-grade corporate credit spreads are expected to remain range-bound in the near term. U.S. high yield bonds face significant economic headwinds and high yield credit spreads may feel the pressure of increasing defaults, downgrades, and bankruptcies. Caution is thus warranted. In emerging markets, the pandemic continues to weigh on fundamentals, but dovish central bank policies remain supportive. Broadly speaking, high quality fixed income should continue to play a useful role in managing overall portfolio risk.

This Newsletter was produced for Middleburg Financial by Capital Market Consultants, Inc.

Sources: Department of Commerce, Department of Labor, Morningstar, Bloomberg, European Central Bank, Institute for Supply Management, National Federation of Independent Business

Disclosures:

Past performance quoted is past performance and is not a guarantee of future results. Portfolio diversification does not guarantee investment returns and does not eliminate the risk of loss. The opinions and estimates put forth constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

Securities are not insured by FDIC or any other government agency, are not bank guaranteed, are not deposits or a condition to any banking service or activity, are subject to risk and may lose value, including the possible loss of principal.

Contact Us